July 15, 2026

Sovereign AI Infrastructure: Why On-Prem Is Coming Back in 2026

For five years, the default answer to 'where does our AI run?' was 'in the cloud, in the US'. In 2026, that answer is getting reconsidered — by procurement teams, by regulators, and increasingly by boards. Sovereign and on-prem deployments are the fastest-growing segment of enterprise AI infrastructure spend.

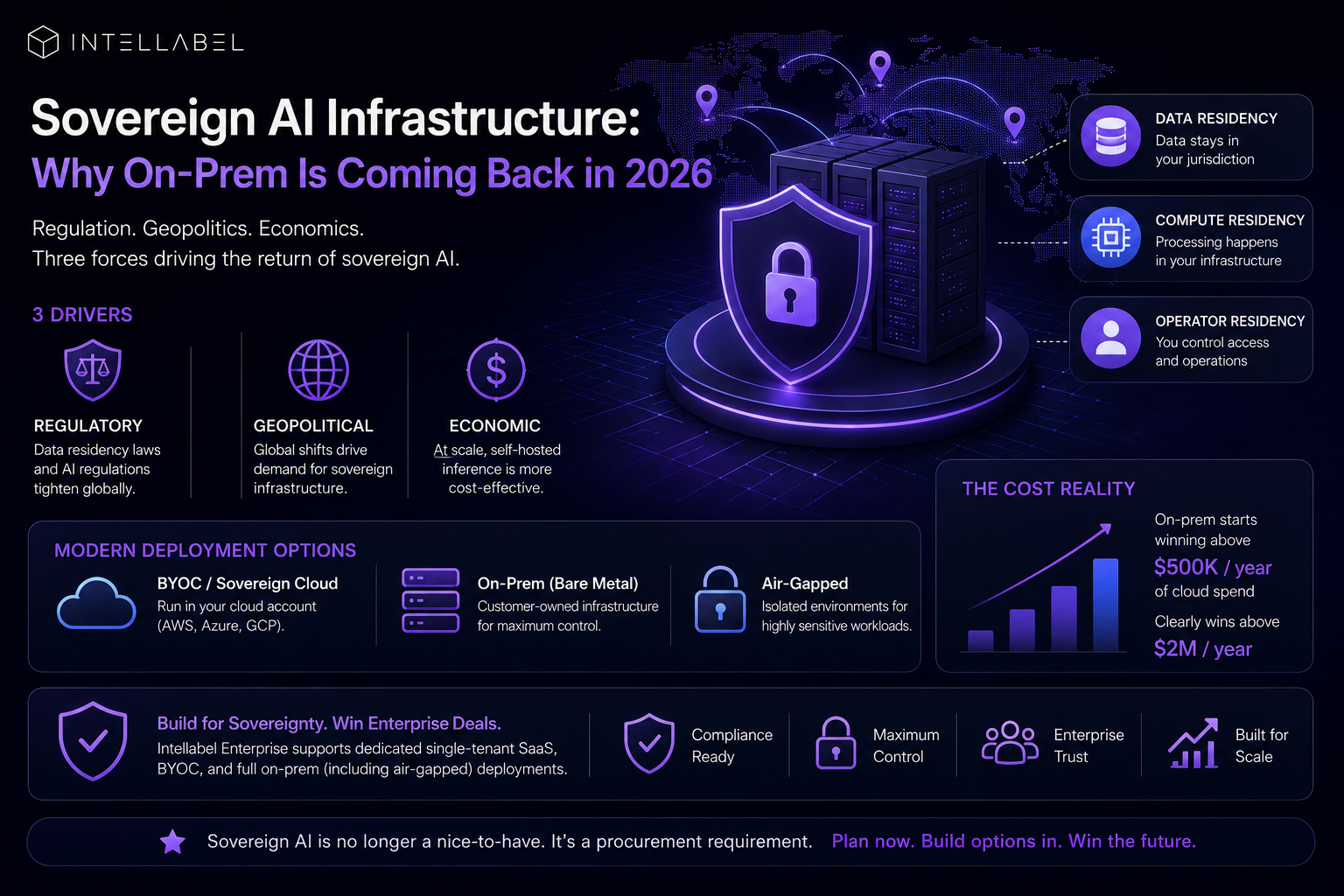

Three drivers

The first driver is regulatory. EU AI Act's data residency expectations, India's DPDP Act, the UAE's data protection regime, and several US state-level AI bills all push toward data-stays-in-jurisdiction defaults. The cost of moving data across borders for AI training is no longer just network egress — it's compliance scope.

The second is geopolitical. The 2024 Meta-Scale AI transaction made enterprise customers in Asia, Europe, and any non-US-aligned market more cautious about US-headquartered AI infrastructure vendors. Sovereign-cloud and on-prem options are the procurement-team-safe answer.

The third is operational. Foundation model API costs at scale exceed the cost of self-hosted alternatives once volume crosses certain thresholds. Companies running 10M+ inference calls per month are increasingly bringing inference in-house.

What 'sovereign' actually means

Sovereign infrastructure means three things together: data residency (where data is stored), compute residency (where processing happens), and operator residency (who has administrative access). All three need to be in scope to satisfy a procurement team — partial sovereignty (data stays in EU but USheadquartered staff can access it) often doesn't pass review.

Most cloud providers offer regional data residency. Few offer all three. On-prem deployment is the simplest way to satisfy all three at once.

What on-prem deployment looks like in 2026

Modern on-prem doesn't mean racks in your basement. The pattern that works: containerized AI platform deployed to customer-owned infrastructure (their VPC, their colo, their data center), with operator access managed by their IAM. The vendor ships software, customer operates.

Three deployment substrates dominate: Kubernetes on customer cloud (BYOC), bare-metal on-prem in regulated industries (financial services, defense, healthcare), and air-gapped deployments for classified work.

The cost reality

On-prem isn't cheaper than SaaS at small scale. The infrastructure cost is similar; the operational overhead is higher. On-prem starts winning above ~$500K/year of cloud spend, and clearly wins above $2M/year. Plan accordingly — don't move to on-prem if your AI workload is small.

The reason organizations move anyway is procurement compliance. The cost difference is borne to unlock customers that won't sign without sovereignty guarantees.

What to build into your platform decision

If your AI vendor doesn't support on-prem or sovereign-cloud deployment, you'll lose a class of customers in 2026-2027. Not most customers — but the largest deals, in regulated industries, on contracts that fund years of growth.

Intellabel's Enterprise tier supports dedicated single-tenant SaaS deployment, BYOC into AWS / Azure / GCP customer accounts, and full on-prem deployment with air-gapped option. The configuration matters less than the optionality — having the choice on the table changes which customers will engage.

The conversation worth having

Sovereign AI is the next regulated AI. The companies that build it into their platform now will close the enterprise deals that companies relying on US-public-cloud-only architectures will lose. Two years ago this was a fringe consideration. In 2026 it's a default question on the procurement checklist.

From Labeling to Structured AI Data Pipelines

Address: WeWork, Salarpuria Symbiosis, Bannerghatta Rd, Bengaluru, Karnataka

.png)